Crypto economy surprisingly resilient to Coronavirus crisis

Despite record unemployment rates wrought by COVID-19, the crypto industry seems resilient—with blockchain jobs, productivity and token sales on the rise.

Add Decrypt as your preferred source to see more of our stories on Google.

In brief

The blockchain and cryptocurrency industry is proving remarkably resilient to COVID-19.

Jobs are plentiful, order books are full and token sales are reappearing.

Industry leaders, such as Chainlink's Sergey Nazarov, believe that a well-defined remote work process is a key part of their business.

A record 6.65 million people filed for unemployment benefits in the United States last week. It’s a similar story across the globe. But the crypto industry is an outlier, and is proving remarkably resistant to the economic fallout of the covid-19 pandemic.

So how do we explain crypto’s resilience in the face of prevailing trends? Where other sectors are faltering, crypto exchanges Coinbase, Kraken and Binance have gone on hiring sprees; crypto-related jobs on Linkedin have seen a continued uptick; and crypto order books are abundant.

Crypto exchanges buck the prevailing jobs trend

Even as the price of Bitcoin and other cryptocurrencies was tanking last week, Kraken, one of the largest cryptocurrency exchanges in America, was on a hiring spree—looking to increase its job force by almost 10%.

It was a similar story for Binance. Barely a week goes by without the biggest exchange by market cap announcing a new product, acquisition, partnership or deal. Just this week, Binance announced it had acquired leading crypto data site CoinMarketCap, in a deal reportedly worth $400 million.

The exchange is looking to fuel its worldwide expansion, and hiring data product directors, managers, UX and UI designers, and researchers—throughout the world.

Unsurprisingly, with coronavirus lockdowns in place across much of the globe, almost all the current jobs on offer are remote. But that’s nothing new for Binance. From cloud-based servers to a distributed workforce, it’s always favored a decentralized approach, and has even been criticized for it.

Oh, so this is what decentralized organization looks like in BCH scene. Very cost effective and practical.

Dovey Wan was onto something, when she said any coffee shop could be a Binance office.

Geography and Covid-19: no barrier for the crypto industry

Nobody’s mocking Binance for its remote-first approach now. It’s not alone in the industry; most blockchain and cryptocurrency firms have a long established practice of employing people in diverse locations.

They’ve found that geographic boundaries and time zones present few barriers to forming cohesive teams, capable of delivering complex projects.

"As a truly open source community driven product/project, we've always been a remote work team,” Sergey Nazarov, CEO of SmartContract, told Decrypt.

The startup is behind the decentralized oracle provider Chainlink, and has a dozen job openings listed on its site. Nazarov considers that a well-defined remote work process is a key part of what they’ve been able to achieve so far.

“We initially went down the remote work path in order to ensure that we have the best people working on Chainlink, wherever they may be and whenever they can find time to do great work together with us,” he said. “This approach seems to have an added benefit in this unique situation, where we've possibly even seen an increase in productivity.”

The Chainlink family before Sheltering in Place became a necessity. (Image: Chainlink)

That’s partly due to the fact that much of the team is now spending less time at crypto events, and more time finalizing launch and implementation details with its growing user base, he added.

Crypto firms report increased orders and activity

Nazarov is not the only CEO tentatively suggesting an uptick in activity. Pascal Gauthier, who heads up hardware wallet Ledger, said that in the first three months of this year, the startup saw double digit growth compared to last year.

Notably, he reported that on March 15, the day the Federal Reserve cut rates to zero and launched a massive $700 billion quantitative easing program, Ledger’s "Nano X mirrored [a] record sales day during the bull market.”

The industry has even revived its practise of raising funds through token sales—increasingly disparaged throughout much of 2019.

A private token sale by the Keep Network, which is developing a Bitcoin-Ethereum bridge,raised $7.7 million, the project announced on Thursday.

Andy Bromberg, cofounder of CoinList, a platform for digital asset companies to run their token sales, highlighted a recent auction event for Solana, a blockchain platform that’s optimised for throughput.

“The Solana auction was the first held amidst COVID-19 and it went very well, clearing $1.76m,” he said, adding that the startup has another token sale coming up soon.

Linkedin ranks the most in-demand skills in 2020. (Source: Linkedin)

Meanwhile, Brian Norton, COO of MEW (MyEtherWallet), a popular interface for the Ethereum platform, claimed great takeup via payment enabler Simplex, which allows customers to buy crypto with a credit card.

“This past week MEW has seen the number of ‘buy’ orders double, coming through on Simplex. With the amount of ETH being purchased jumping nearly 9X over our weekly average,” he said.

Some crypto firms fall foul of COVID-19

However, it’s not all been plain sailing for the crypto industry in the midst of the coronavirus pandemic.

The first big crypto casualty was Factom, one of the first crypto companies to launch an initial coin offering (ICO). On Thursday, it was announced that the startup had gone into liquidation.

Factom raised $140,000 in Bitcoin in August 2015—equivalent to around $4 million at today’s prices—and an additional $18 million from investors over the past five years. A grant from the US Energy Department to use the blockchain to secure the nation’s power grid—and its use by the Department of Homeland Security and the Bill Gates Foundation—were not enough to save it.

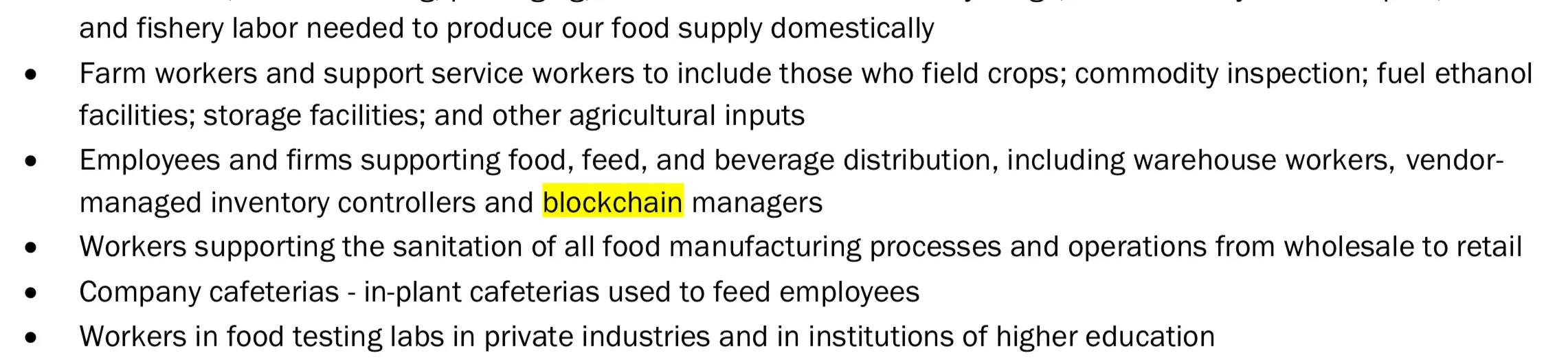

The US Department of Homeland Security Cybersecurity and Infrastructure Security Agency lists blockchain managers as “Critical Services Workers” in its COVID-19 Response. (Source: CISA)

An industry prepared for a post-coronavirus future

On the whole, though, the decentralized nature of the crypto business has shielded many companies from the worst of the economic fallout.

The boom in digital assets trading over the past two months is continuing to drive wallets, exchanges and other infrastructure providers to increase their employee headcounts.

A quick scan of cryptocurrencyjobs.com and cryptocareers.com reveals over a thousand openings at large-scale startups such as decentralized crypto browser Brave and Cardano developer IOHK, as well as smaller, early-stage startups like Synthetix.

Getting used to work from home, but hate your job?

And the privacy-centric nature of many crypto projects leaves them well-placed to respond to one of the key issues taking centre stage during the pandemic, the use of private and government surveillance to curb the spread of coronavirus.

Crypto events, meanwhile, have seamlessly moved online, with dozens of virtual conferences announced.

What hasn’t changed is crypto’s decentralized ethos, which sits at the very heart of the majority of projects. It’s stood the industry in good stead so far.

Daily Debrief Newsletter

Start every day with the top news stories right now, plus original features, a podcast, videos and more.