The ongoing liquidity issues at crypto lenders BlockFi, Celsius, and Voyager Digital have put other crypto lenders in the hot seat, with some rushing to assure clients that their funds are safe.

But Nexo, which points to its real-time attestations from accounting firm Armanino as proof that it hasn’t gone the way of its competitors, has also had to contend with a Twitter user who claims its co-founder Kosta Kantchev embezzled funds from a charity to build “a palace the size of a high school.”

In response to those claims, the company has printed a rebuttal that dismissed the accusations as a case of mistaken identity, writing that the account has been using “lies and distortion in yet another smear campaign against Nexo.”

The company’s legal department got involved too, sending a cease and desist letter to the person running the Twitter account.

“He claims a lot of things, but that we are insolvent. is not one of them,” Nexo co-founder and Managing Partner Antoni Trenchev told Decrypt. “It’s a prediction that we will be insolvent by the end of the year, and they haven't backed this up in any meaningful way.” (Disclosure: Nexo is one of 22 investors in Decrypt.)

Nexo will undergo a liquidity crisis by the end of 2022 (87% certain)

Of all the CeFi lenders covered, Nexo is the champ in half truths and illusionary otter tactics

Read on as otter uncovers the tricks!

(Part I of II)

🦦 👇🏼 🧵

— otteroooo (@otteroooo) June 22, 2022

Trenchev said that Nexo only appears to be like its crypto lending competitors, which typically take client funds and stake them in yield-generating protocols or make what he considers under collateralized loans. Nexo is fundamentally different, says Trenchev, and hasn’t had to resort to any of the same measures to stay afloat.

Those measures include freezing or limiting withdrawals, like Celsius, or seeking a revolving line of credit, like BlockFi. Voyager has had to do both.

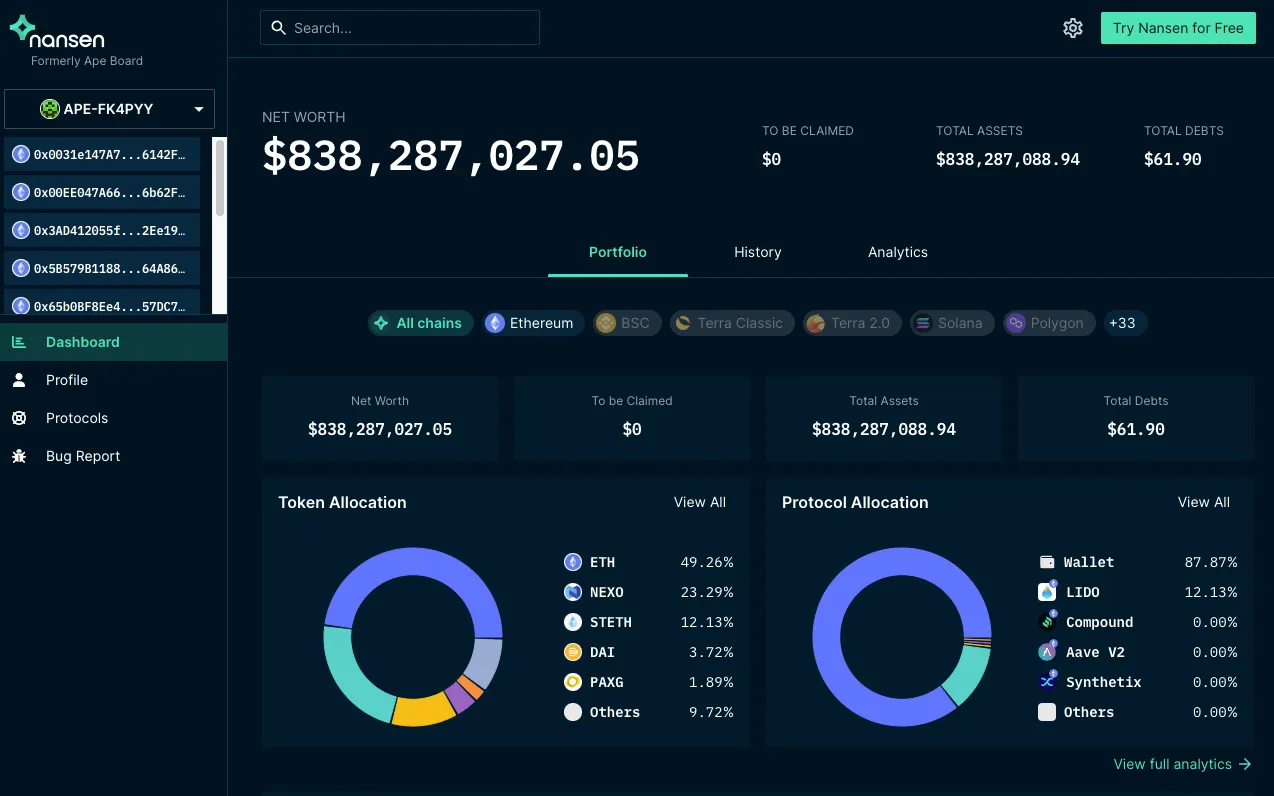

Like its competitors, Nexo loans out client funds and uses the proceeds to pay interest. Blockchain analytics platform Nansen has identified more than 500,000 wallets as belonging to Nexo.

That includes one that Nansen has identified as Nexo’s corporate treasury. It had a balance of $169 million as of Tuesday morning. The majority of the funds, $104 million, was in Staked Ethereum (or stETH)—that is, ETH that's been locked up on the Ethereum 2.0 beacon chain through service provider Lido.

Nansen CEO Alex Svanevik shared a dashboard with Decrypt showing that several of Nexo’s largest wallets, including its $169 million on-chain treasury, have a balance worth $838 million. Half of that was being held as ETH and a quarter as the company’s native NEXO token.

Another of the company’s wallets included in the Nansen dashboard showed that Nexo had deposited $579 million worth of Wrapped Bitcoin (wBTC) as collateral in a MakerDAO vault and had an outstanding balance of $50 million DAI.

All of this is to say that a sizable portion of capital sitting in Nexo wallets is being held as ETH, stablecoins, or been lent out to protocols that require loans to be overcollateralized.

Unlike its competitors, Nexo says it only makes overcollateralized loans. That means it tends to pay lower yields than BlockFi and Celsius, but exposes clients to “basically no risk,” according to its website.

Trenchev said Nexo hasn’t used funding from investors to meet its client obligations, another detail he said sets it apart from other crypto lenders.

“We have invested while times were good for the space,” Trenchev said. “During that time, 18 months I think it took us, we worked with Armanino, which is a top 20 auditor in the U.S., to develop a real-time attestation that our assets exceed our liabilities by more than 100%.”

The company has also been working with several investment banks—one of them Citigroup—to explore opportunities to acquire struggling companies.

“It is essentially up to us to do our best to help clean up the space in a sort of consolidation effort,” Trenchev said.

Lately, it’s often been the case that when one big player in a crypto category falls, its peers draw scrutiny simply because they appear to have similar businesses.

It happened to stablecoins after TerraUSD (UST) lost its peg and went to zero. Tether (USDT) and Circle’s US Dollar Coin (USDC) were quick to draw a line in the sand to separate their stablecoins, which are purportedly backed by an equivalent reserve of U.S. dollars, from Terra’s algorithmic coin, which was originally backed by nothing at all and then later a mix of other cryptocurrencies, including Bitcoin.

Case in point: Tron’s algorithmic stablecoin, USDD, which founder Justin Sun has said is safer than UST because it’s overcollateralized, has been off its 1:1 peg with the U.S. dollar since June 12. On Monday afternoon, it was trading at $0.98, according to CoinMarketCap.

After Terra’s fall, there was a rush from its investors, venture capital firms, to say whether they had any exposure. Over the course of a few weeks, disclosures came from Galaxy Digital CEO Mike Novogratz, Dragonfly Capital, Multicoin Capital and others.

The problem that Nexo is facing, trying to distinguish itself from other crypto lenders, is one that Armanino set out to solve with its TrustExplorer product.

The company is able to check the balances in its clients’ bank accounts and crypto wallets daily, compare that to its liabilities, or money it owes its clients, and assess the health of the lending business. For example, as of Tuesday, Nexo had assets in excess of its $4.3 billion customer liabilities, according to the TrustExplorer report.

The idea is that the transparency will help companies avoid what’s happened at Celsius, where Noah Buxton, an Armanino partner, told Decrypt there’s been an asset-liability mismatch and maturity problem—all at once.

He said that’s the problem the team behind TrustExplorer, which started out as a tool for verifying the reserves backing stablecoins, has focused on as they adapted it for lenders. In fact, it’s Nexo that prompted them to do it in 2021.

“[Lenders] have notes with counterparties. They have assets listed on the global exchanges, they have some DeFi exposure as well,” Buxton said. “So we're looking at a number of things on the asset side, probably, honestly, 50 different sources of assets that we pull in, but then that one liability matching the two.”

While Armanino’s attestations may set Nexo apart from other lenders and provide some comfort to crypto market observers, it’s important to note that attestations are not the same thing as audits. And given the current state of the market, it’s not hard to understand the growing skepticism of the crypto lending market as a whole, including Nexo.

That skepticism isn’t lost on Nexo or its accounting firm. “Nobody trusts anybody, even though you're showing them the proof in their face,” Buxton said.

Editor's note: An earlier version of this article noted Nexo's on-chain treasury, but not it's off-chain assets, which a Tuesday TrustExplorer report said are in excess of its $4.3 billion customer liabilities.