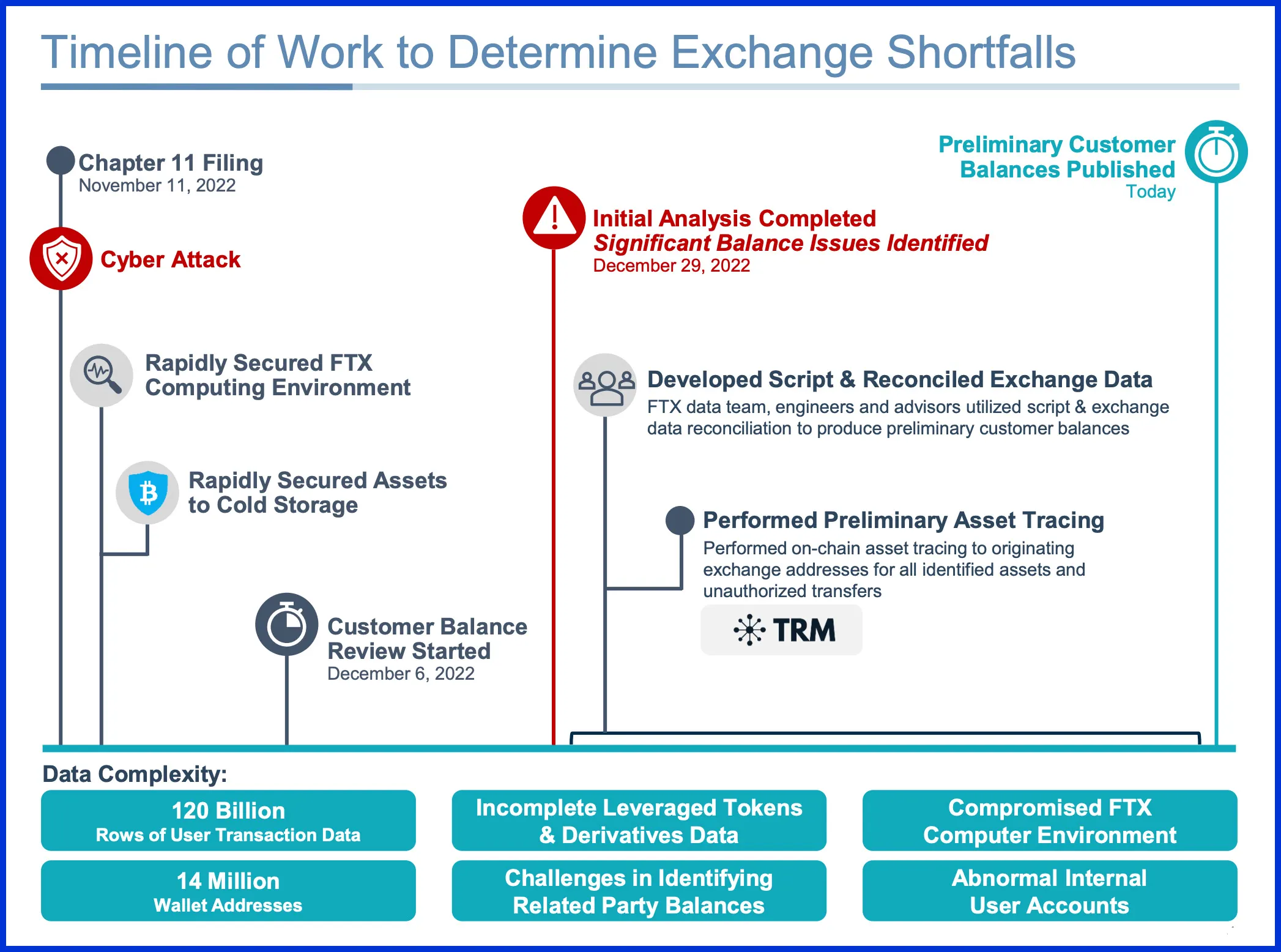

A concerted effort to identify and inventory the remaining assets of failed cryptocurrency exchange FTX has revealed "the magnitude of the shortfalls discovered in the fiat bank accounts and digital asset wallets associated with the FTX.com and FTX.US exchanges," according to a presentation filed by FTX Debtors in the firm's Chapter 11 bankruptcy cases Thursday.

$2.2 billion of total assets have been located, according to the presentation, of which only $694 million are the most liquid currencies, such as fiat, stablecoin, BTC or ETH. Against these holdings—and another $385 million in customer receivables—are $9.3 billion in net borrowing by Alameda Research.

And FTX CEO John J. Ray III warned that all the facts are not yet in.

"It has taken a huge effort to get this far," Ray said in a press release. "The exchanges' assets were highly commingled, and their books and records are incomplete and, in many cases, totally absent."

In fact, the presentation states that the information provided is preliminary and "should not be relied upon for any purpose." But Ray, who also serves as chief restructuring officer of the FTX debtors group, said sharing the latest information was a priority.

"We believe it is more important to provide transparency to stakeholders by making this information public now than to wait until we can achieve certainty," he said.

While disgraced FTX founder Sam Bankman-Fried has repeatedly claimed that FTX US "fully solvent," the debtor group's research says otherwise.

"$191 million of total assets have been located today in the wallets of the accounts associated with the FTX.US exchange, in addition to $28 million of customer receivables and $155 million of related party receivables," the group states. "This compares to $335 million of customer claims and $283 million of related party claims payable."

"Unauthorized transfers removed an additional $293 million from wallets preliminarily sourced to the FTX.COM exchange and $139 million from wallets preliminarily sourced to the FTX.US exchange," the presentation noted.

The presentation also updated the amount of liquid assets currently recovered and held by the debtors group, which grew from $5.5 billion to $6.1 billion since its last report in January. Although the increase is primarily the result of updated digital asset pricing, the group also recovered $202 million held at Alameda, $125 million in stablecoins, and $57 million in assorted cryptocurrency held at subsidiaries.

Despite the information gathered to date, the FTX debtors group attached numerous disclaimers to its report, noting that "it is not possible to calculate or predict customer recoveries based on the preliminary information in the presentation." Reasons cited include fluctuating valuations, insider access, commingling of funds, other unidentified claims, and the disposition of "over a hundred companies comprising the FTX group globally."

"The analysis is further complicated by the incomplete nature of the books and records and financial information maintained by pre-petition management," the group adds. Ray has previously decried the misdeeds of “a very small group of grossly inexperienced and unsophisticated individuals” who were at the helm of FTX.

Finally, the debtors group revealed more information on daily deposits and withdrawals from both exchanges during the 90 days prior to the commencement of the chapter 11 cases for the exchanges. While the figures unsurprisingly show a spike in withdrawals just prior to FTX's bankruptcy filing, they also show a spike in deposits attributed to deposits from Alameda.

Today's presentation and filings are only the latest update in the still-unraveling FTX saga.

"This is the second in what the FTX Debtors anticipate will be a series of presentations as we continue to uncover the facts of this situation," Ray wrote.