Tranching Helped Fuel 2008 Financial Crisis. Now It’s Coming to DeFi

In a newly released report, ConsenSys Codefi pointed to a coming DeFi innovation that demonstrates the benefits and risks of building financial instruments with money legos.

In its recently released 2020 Q4 review, ConsenSys Codefi, a product suite for commercial applications of decentralized finance (DeFi), took a trip down memory lane, chronicling the developments of October through December.

And then it looked ahead to 2021 by throwing something crazy out there: tranche lending.

If you haven’t heard of it, tranche lending is a method of tackling variable interest rates in DeFi, the suite of tools that allow people to access loans, earn interest, and swap assets without a financial institution’s say-so. Outside of crypto, tranches were used in the mortgage-backed securities that helped fuel the 2008 financial crisis.

Read our new deep dive into the biggest trends in decentralized finance. 📝

What we cover: ✅The fast rise of stablecoins ✅ Bridging centralized & decentralized finance ✅ Eth2.0 derivatives ✅ DAOs ✅Flashloans ✅NFT Marketplaces

A tranche, explained report authors James Beck and Tom Hay, lets users deposit assets that are then lent out to other users “via lending protocols such as Aave or Compound” —but they get to decide how risky the pool is. For example, deposits into Tranche A might receive a fixed interest rate, whereas deposits into Tranche B can earn extra interest if the realized APY goes above that fixed rate...or less if it falls below.

In other words, tranches allow users to choose a sure thing or gamble on more.

BarnBridge and Saffron Finance are two protocols getting ready to roll out tranche lending.

BarnBridge co-founder Troy Murray told Decrypt it expected to release its products this quarter, pending external audits. Saffron Finance has not yet been audited.

AD

AD

As Beck and Hay note, “Tranche lending exemplifies just how composable all of these innovations are. The teams who devised this tranche lending system did not come from Compound or Aave, yet they built an entirely brand new product on top of the existing lending protocols.”

There is a looming downside from that composability, however. In the runup to the 2008 financial crisis “tranches of junk mortgage-backed securities were repackaged as CDOs, further sold.” CDOs, or collateralized debt obligations, were agreements to pay investors based on their tranche. Tranche A would get funds first, for instance, while the tranches down the line would be likeliest to lose out.

That seemed okay, but such financial products didn’t exist in vacuums; they were impacted by other economic forces.

“The more that various financial products rely on one another, the more intertwined the risks of these products become,” Beck and Hay wrote. “If one of the underlying protocols fails, they present a systemic risk to the other related products that interact with the protocol.”

BarnBridge's Murray believes many of the problems in 2008 really came not from financial instruments, but from the credit agencies—organizations typically paid by the security issuer to assess the risk of the process.

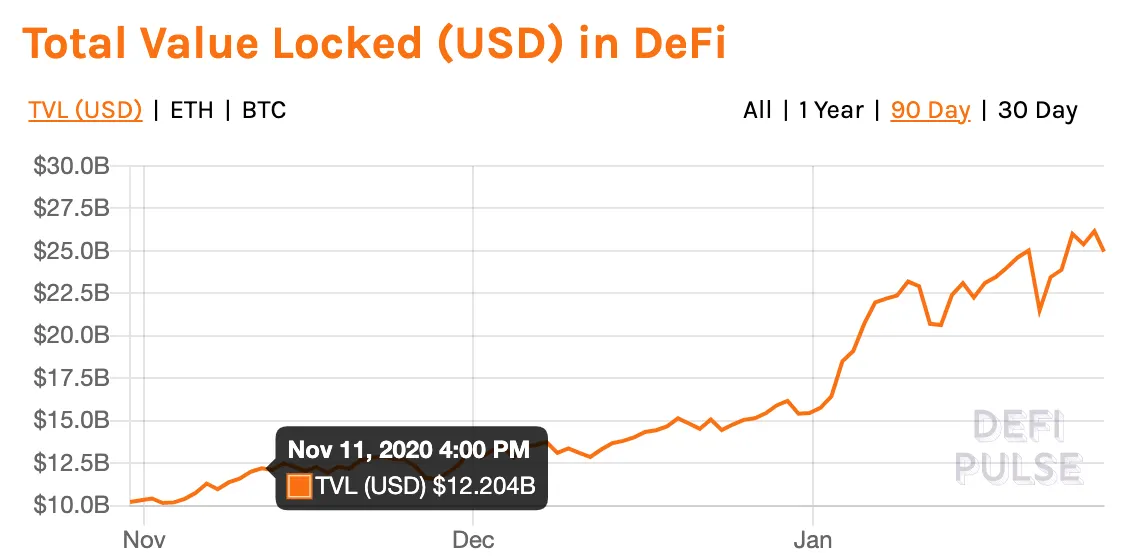

Total value locked in protocols listed on DeFi Pulse over last 90 days. Source: DeFi Pulse

“In a system that can be audited on the fly like DeFi a lot of that risk is mediated out because you don't have a central player who can be corrupted to rate something one way or another because their incentives aren't aligned correctly,” he told Decrypt. “Which is what happened in 2008. If anything DeFi is a huge improvement on that. It wasn't the financial instrument that was bad, it was the bad human actors.”

Either way, say Beck and Hay, humans need to understand how these products work, given how complex they are.

In fact, they wrote, it’s “imperative in order to avoid significant financial loss.”

AD

AD

(Disclosure: ConsenSys provides funding to an editorially independent Decrypt.)

Stay on top of crypto news, get daily updates in your inbox.