We do the research, you get the alpha!

The wide-ranging repercussions of May’s devastating crypto crash are still being accounted for.

In a quarterly earnings report released yesterday, Bitcoin mining firm Stronghold revealed that it had reached an agreement with lender New York Digital Investment Group (NYDIG) and another participating broker, to return some 26,200 mining machines in exchange for the cancellation of $67.4 million in debt.

Additionally, Stronghold received a commitment yesterday from lender WhiteHawk Capital to restructure and expand its current equipment financing agreements, in a move that will grant the Bitcoin miner up to $20 million in additional borrowing capacity.

All in all, those agreements—combined with a convertible notes restructuring—will reduce Stronghold’s debt by $79 million.

That’s 55% of the company’s current debt; $64 million will remain outstanding.

Bitcoin miners brace for bear market

The move comes as crypto companies continue to take stock of the crippling impact of May and June’s crash, which in many regards still persists.

Though Bitcoin temporarily recovered to $25,000 recently, the leading cryptocurrency is still down 65% from its November 2021 peak of $69,044.77. Bitcoin currently sits at $23,821.80, according to data from CoinMarketCap.

That massive downswing has devastated Bitcoin miners like Stronghold, which pay huge overhead equipment and energy costs to produce the blue-chip cryptocurrency.

To survive the crash, other Bitcoin miners have taken to selling their Bitcoin reserves, a surprising move for some of the industries most die-hard HODLers.

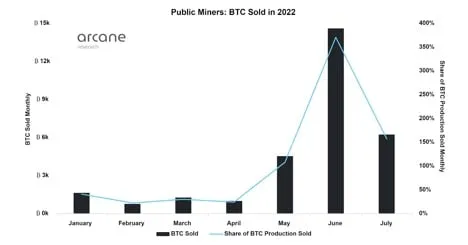

According to a report from Arcane Research, Bitcoin miners sold off almost 15,000 BTC in June, a whopping 400% of their Bitcoin production. That number eased off in July, down to 6,200 BTC.

Still, that’s 158% of the Bitcoin produced by these miners, an indication of dire financial straits.

As opposed to selling off its Bitcoin supplies, however, Stronghold reduced its debt by selling off mining equipment. The company is insistent this will not impact its long-term BTC production capacity.

Greg Beard, Stronghold’s co-chairman and CEO, said in a statement that the company’s current position “provides additional availability for us to patiently and opportunistically acquire Bitcoin miners at currently depressed prices.”

He also alluded to alternative income streams that could keep the company generating revenue in the meantime.

“Our power generation capacity remains unchanged, so, while our Bitcoin mining fleet has been reduced in the short run, we have significantly more open exposure to strong power markets,” said Beard. “Forward prices suggest that selling power is an attractive alternative to Bitcoin mining, irrespective of the size of our mining fleet.”

Stronghold’s stock fell 17.55% yesterday upon disclosure of the mining equipment sell-off. The stock has fallen a stark 75.76% year to date, and is trading at $3.19 at writing.